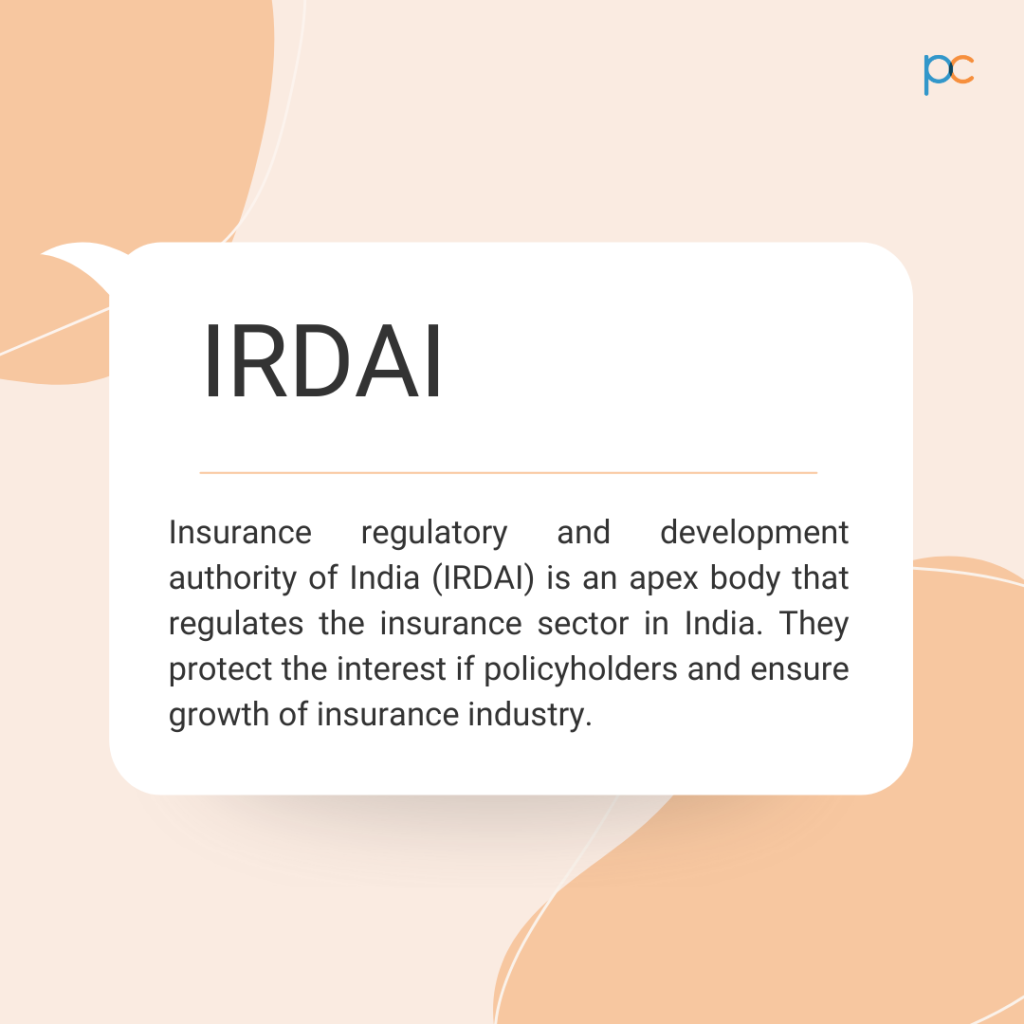

IRDAI, the Insurance Regulatory and Development Authority of India, regulates the insurance companies that function in the country. Whether you go for group health insurance or an individual one, IRDAI sets the guidelines associated with it. Read along to know the guidelines set by IRDAI for the employer or group health insurance plans in India.

Table of Contents

A brief outline

Before getting into the guidelines in detail, understand what a group healthcare plan is. A group health insurance plan is for the employees in an organization, offered by the employer of the company.

Startups, businesses, and companies all-over India can qualify for buying the policies for their employees. Informal groups can also purchase the policies where the group members can enjoy plan benefits. In an employer-employee group, the employer pays the premium for which the employee and their family members (subject to inclusion) can enjoy the medical expense coverage under the insured sum limit.

The policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More benefits are active till the last day of service. If the employee leaves the organization or group, the group policy gets cancelled. If they want, they can port it to an individual policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More under the IRDAI guideline and continue paying the premiums for enjoying the benefits.

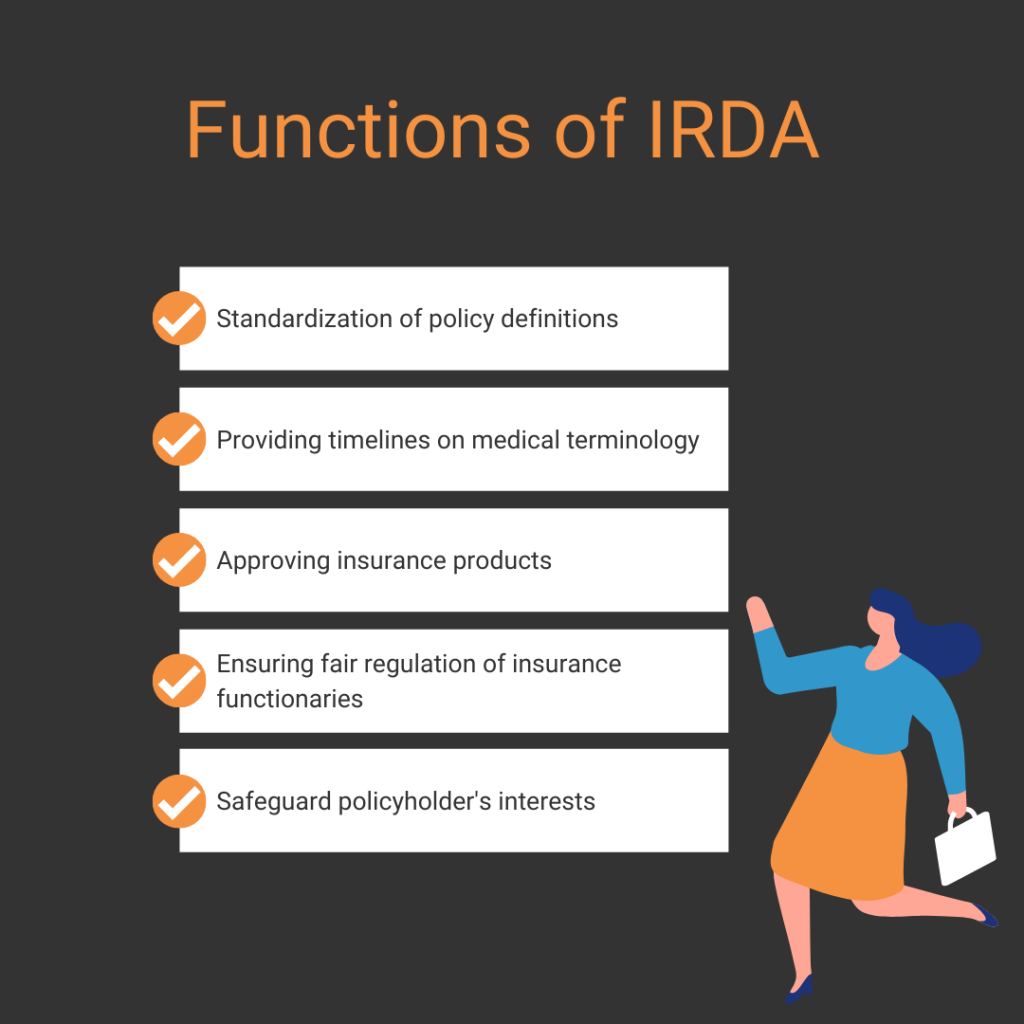

Guideline on medical terminology – As there are multiple facets related to medical treatment, it is crucial for the insurance regulatory body to define certain terms for the benefit of the insurer. With the specified guidelines and standard definitions, it gets easier to understand the coverage and non-coverage aspects.

Every insurance provider has to adhere to the IRDAI standard definitions and terminology related to all products filed under Health Insurance Business. Thus, group health insurances also have to operate as per the defined terminology norms and regulations.

- AccidentAn accident refers to an unforeseen, unintentional, and unexpected event that occurs suddenly and results in injury, damage, or loss. More – Refers to an unforeseen, sudden and involuntary event. As per the guideline definition, the accidentAn accident refers to an unforeseen, unintentional, and unexpected event that occurs suddenly and results in injury, damage, or loss. More has to be an impact-induced by an external and visible violent means.

- Any one illness – Refers to the continuous course of illness and also includes the relapse of the disease. The relapse should be within 45-days and counted from the last day of medical consultation in the hospital, where the policyholderA policyholder is an individual or entity that owns an insurance policy and pays the premium in exchange for coverage. More was admitted.

- Cashless facility – Refers to the facility where the insurer pays for the cost of treatment and all associated payments to the hospital where they are admitted. The facility gets followed as per the specific policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More terms and conditions and is directly paid to the network provider.

- Condition precedent – By the definition, it refers to the policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More condition on which the insurance provider’s liability is conditional.

- Congenital anomaly – The health conditions present in the body since birth falls under the definition. It can be internal or external.

- Copayment – Refers to the provision of cost-sharing in a healthcare plan. Through copayment provision, the policyholderA policyholder is an individual or entity that owns an insurance policy and pays the premium in exchange for coverage. More can share a specific percentage of the claim amount. It does not affect the sum insured.

- Cumulative bonus – Refers to the increase in the insured sum granted by the insurer without increasing the premium.

- Day-care treatment and center – Medical day-care treatment which lasts around 24hours, gets covered through a group healthcare insurance scheme. It may include treatment procedures like – chemotherapy, hemodialysis, radiotherapy, etc. Any treatment process lasting less than 24hours that may require medical observation for 24hours or less gets included in plan coverage.

- Deductible – Deductible refers to the cost-sharing requirements for which the insurance provider will not be liable to pay. It can also be a specified amount in the case of indemnity policies and is also applicable for a specific number of hours or days in the case of cashless hospital expenses. It depends on the insurer if the deductible is valid and applicable per year or throughout the insurance course.

- Domiciliary treatment – Refers to the treatment of disease/injury that takes place in the residence of the patient. It may be covered by the insurer under certain conditions like – the patient is in an unsuitable condition to move to a hospital for treatment or there is an unavailability of room in the hospital for carrying out the treatment.

- ICU and critical illness – The identified section or wing in the hospital where the patient is kept under the supervision of a medical practitioner(s). A patient in the ICU is in a critical condition and needs life support facilities and continuous monitoring. The supervision and care in the ICU wards are more intensive than in other hospital wards. The expense covered by the insurer for the ICU ward includes charges for ICU beds, general medical support, monitoring devices, etc.

- OPD treatment – OPD treatment and regular medical checkup expenses have distinct norms. The insurance should reimburse the cost for OPD treatment. However, the claim amount is limited and pre-defined in the insurance plan. For regular checkups, the insurance company is not bound to bear the expense. Of late, some insurance companies are providing such benefits to attract customers.

Other aspects mentioned in the guideline

The IRDAI guideline on standardization of health insurance has several definitions and norms mentioned. The above-discussed terms are from the IRDAI guideline and are frequently required by the policyholderA policyholder is an individual or entity that owns an insurance policy and pays the premium in exchange for coverage. More while filing a claim or getting a cashless facility. You can learn more about the definitions by going through the guideline circular.

Besides these, there is a dedicated chapter in the IRDAI guideline to discuss the standard nomenclature and procedure for critical diseases and illnesses. With the 22 critical diseases and medical conditions discussed in the guideline, it gets easy for the insurer to define the coverage expectations in their policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More book. The second chapter covers the following – Specifications of coverage norms related to cancer and its severity, myocardial infarction, COMA of specified severity, kidney damages and illnesses that need dialysis, organ transplant, permanent limb paralysis, motor neuron disease, etc.

PolicyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More benefits you get with the group healthcare plan.

In a group healthcare policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More, the employer can pay a premium for the employee and their family members(spouse, children, and dependent parents). The beneficiaries can get cashless treatment and reimbursement through plan expense coverage. However, multiple regulations are there about what is included and excluded in the plan coverage list. The coverage features depend on the insurance company you select, and so does the premium. Every insurer has to follow the definitions and standardization guidelines stated by IRDAI in defining their coverage aspects.

How can you buy one?

As an employer, you can now buy group health insurance for the employees working under you. The sum to be insured depends on the buyer. The employer can also decide if they want to include the family members of the employees into the list. In any of the cases, the employer has to first find a suitable policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More. They can approach the insurance company directly and pick a plan to buy. Or, an employer may reach out to an insurance broker to find the best insurance plan in the market. Insurance brokers offer several group healthcare plans from the leading insurance companies in India.

PlanCover at your assistance

PlanCover offers group health insurance plans for employers. Any small-scale or mid-level organization having 7 to 450 employees can connect to PlanCover and purchase it from them. You can reach out to them and gain a clear idea about the leading plan and premium rates from the IRDAI-approved list of insurance companies. Their expert team can also guide you with authentic information related to healthcare plans and IRDAI guidelines. Get started with the process by connecting to their representatives.