Employees are considered to be the biggest asset of a company. For organizations, employee benefits are key drivers in recruiting and retaining competent talent. Jobseekers often carefully weigh the benefits attached to a prospective work opportunity during the recruitment process.

Most companies purchase group health insurance policies for their employees and in many cases, for the employees’ families. Employers buy health insurance plans for their employees, and the concerned employee is expected to pay a part of the premium. Group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More benefits the employees as they have to pay a lesser premium compared to what they would have to pay if they bought a health insurance policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More on their own.

Table of Contents

What is group health insurance?

Group health insurance, also known as group mediclaim, and corporate health insurance among other terms is a formal contract between an insurance provider and a group of people that are part of a recognized group, a legal business entity, an organization or an association. Under group mediclaim insurance, a single policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More is issued to the group and each member might be given a certificate of insurance.

Now let’s look at who can purchase a group health insurance. Group health insurance is usually purchased by employees and employers groups that are part of a business. Group health plan purchase is common in religious and spiritual bodies and societies, non-profit organizations, and housing societies, among other groups.

Why should companies consider group health insurance plans?

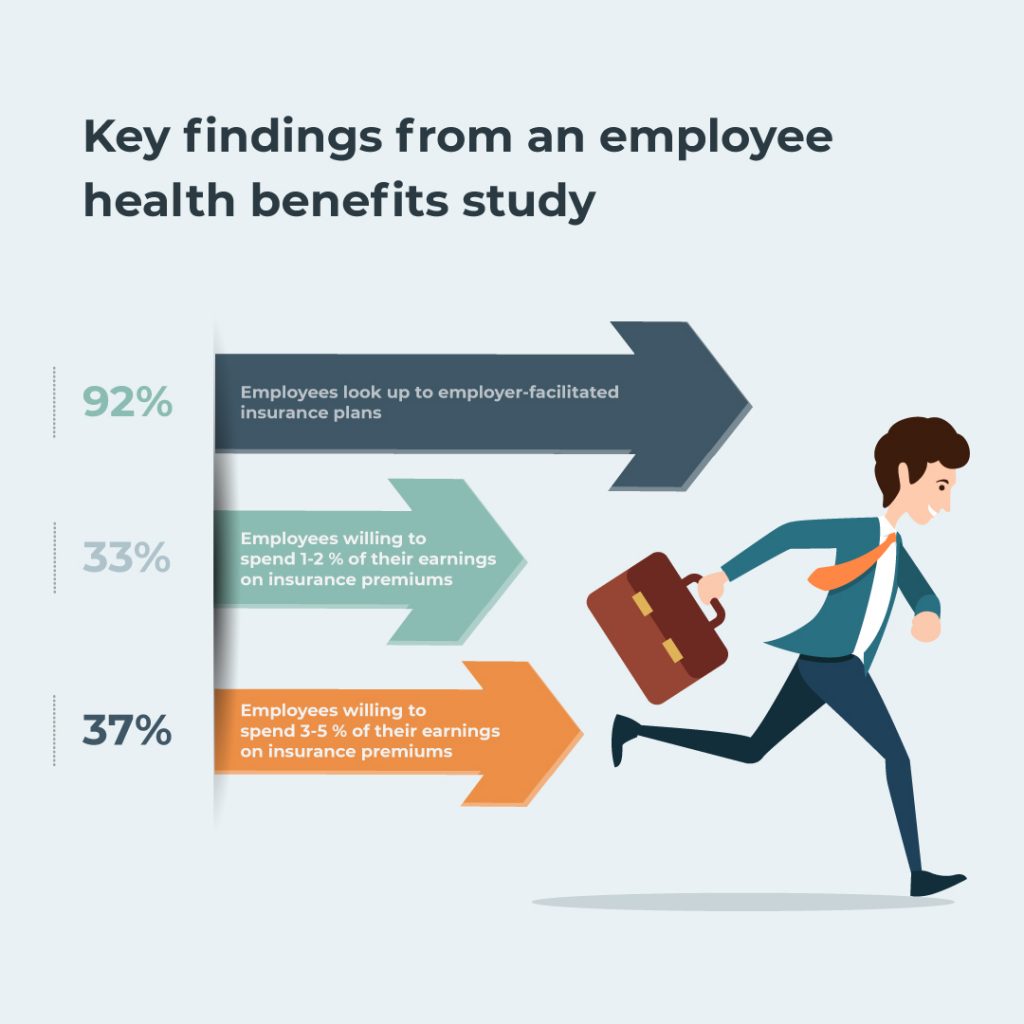

- Group health insurance plans are cost-effective, both for the company and the employees.

- They provide medical expense coverage to the employees and their families, which is a way of showing employees that the company cares for them.

- Employee health benefits have shown a 25% decrease in sick leaves, in worker’s compensation and disability pay.

- 98% of the employees who had health check-ups experience a higher quality of life.

- Purchasing group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More plans may offer tax benefits to companies.

- Employers can help protect the savings of their employees by providing them health insurance.

- Companies can provide quality health care to their employees.

- Businesses face competition and pressure from competitor companies that provide benefits to their employees. Employers could use group health benefits to provide similar benefits.

Determining the most effective group health insurance

Most insurance providers offer group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More plans. However, companies should consider key factors, such as the product, cost, and service, among others, to determine the most efficient group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More policies. Here are a few key factors to consider when choosing a group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More plan.

1. The number of employees

According to the IRDA, a company must have a minimum of 20 employees to be able to apply for a group health insurance policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More. However, this number can vary depending on the insurer. Some insurers provide group health insurance to 10 employees as well.

2. The benefits of group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More for your employees

Companies can ensure they make the right choices of insurance policies by holding discussions and surveys among employees to determine the needs of each employee or different sets of employees. Companies should consider both, the medical requirements and the ability to pay premiums with respect to the employees’ income.

Companies could consider factors such as the employees’ age, family members, medical conditions and salaries and bracket employees in certain predefined categories. Employers can then find the most suitable health plan for the different groups of employees. For example, employers could go for an individual plan that covers only the employee or a triple cover that covers the employee’s spouse and children, for those employees that prefer coverage for their family members, too.

3. The premium and review rates

Just because one insurance plan is cheaper than what another company might be offering, does not mean the cheaper option is better. Employers must consider the kinds of benefits and coverage provided under different plans and rates. A comparative review of a few selected plans from different insurance companies could help employers assess the most suitable plan for their company.

Here’s a tip: Requesting for bids and quotations from at least two or three or more insurance companies would help you determine the suitable policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More.

4. The service provided by the insurance company

It is essential to ensure that the insurance company is providing you with top-notch service. There are many factors to consider here. Is the insurance company prompt in attending to your queries? Do they have helpful customer service?

Here’s a tip: Ask the bidding companies to provide references from within the industry. Speak with the recommenders and clear your doubts.

5. Is there a possibility of tailor-made policies for companies?

Unlike individual policies, organizations do have the option of tailoring the terms of the policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More to meet their employee needs. These are some aspects that group policies can and should look into:

- Coverage for diseases existing during the time of purchasing a policyAn insurance policy is a legally binding contract between an insurance company (insurer) and an individual or business (policyholder). It More

- Policies that do not have a 30-day waiting periodA waiting period in insurance refers to the time frame during which a policyholder must wait before certain benefits become More

- Policies that do not have a waiting periodA waiting period in insurance refers to the time frame during which a policyholder must wait before certain benefits become More of 1 or 2 years

- Policies that provide maternity coverage with or without a waiting periodA waiting period in insurance refers to the time frame during which a policyholder must wait before certain benefits become More of 9 months

- Policies that provide Baby Cover from day 1 of birth, which is otherwise covered after 90 days

- Amount of maternity depending on the kind of delivery – Normal and C-Section

- Policies that include or exclude certain kinds of treatments

- Policies that allow Corporate Buffer. (If an employee expends the sum insured, the management could add an additional amount

- Policies that offer co-payments, where the amount can be borne by the employee as a percentage of claim, which can reduce premiums

Is it time to revive your group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More benefit programme?

The landscape of the Indian job market and workers benefit is changing with new companies entering the market, employees being more aware of the benefits that they can receive at their workplace, and organizations, too, wanting to offer the best to their employees. However, a number of companies still follow the same approach to selecting group health insurance plans. Companies end up opting for the same plans with the same insurance provider that they have been partnering with for years.

Convenience, trust, lack of time or lack of enthusiasm to explore new offerings, whatever may be the reason, a lot of companies that do not revive their employee health benefits programmes could risk losing key talent because of this reason.

Are you an old company looking to revive your company’s group insuranceGroup Insurance is a type of insurance policy that covers multiple individuals under a single plan, typically provided by an More plan? Or are you a startup looking to offer health benefits to your employees? You could explore group health insurance plans offered by PlanCover.