ICU Capping: What It Means for Your Indian Health Insurance

ICU Capping: What It Means for Your Indian Health Insurance

Intensive Care Units (ICUs) offer life-saving support for critically ill patients. However, these specialized units come with hefty price tags. ICU capping in health insurance acts as a safeguard, setting a limit on the amount your insurer will cover for ICU charges during a hospitalization. Let’s delve into what ICU capping entails for both retail health insurance (individual plans) and group health insurance (employer-sponsored plans) in India, with a statistical perspective on healthcare costs.

ICU Capping Explained

- Room Rent Capping: Most health insurance plans in India impose limits on daily room rent charges. ICU capping specifically focuses on limiting the daily amount covered for ICU room expenses.

- Calculating Coverage: ICU capping can be a fixed amount (e.g., ₹10,000 per day) or a percentage of your sum insured (e.g., 1%-2%). If your ICU stay surpasses this cap, you’ll be responsible for the out-of-pocket costs.

Example: ICU Capping in Action (Retail Plan)

Imagine your retail health insurance policy has a sum insured of ₹5 lakhs and an ICU cap of ₹15,000 per day.

- Scenario 1: Your ICU stay lasts for 7 days, with daily charges of ₹22,000 (total ₹1,54,000). Your insurer pays ₹1,05,000 (₹15,000 x 7 days), and you’d be responsible for the remaining ₹49,000.

- Scenario 2: Your ICU stay is for 4 days at ₹12,000 per day (total ₹48,000). The insurer covers the entire cost (₹48,000) as it falls within the limit.

Group Health Insurance and ICU Capping

- Employer-driven Plans: Group health insurance plans offered by employers often have pre-negotiated rates with hospitals, potentially leading to lower ICU charges compared to retail plans.

- Policy Variations: Specific ICU capping details within group health plans can vary depending on the company’s negotiated terms with the insurer. Review your policy documents or consult your HR representative for clarification.

Factors Affecting ICU Costs in India

- Hospital Tier: Costs vary significantly between private hospitals (Tier-1, Tier-2, Tier-3) and government facilities. Generally, ICU expenses are highest in premium private hospitals.

- Geographic Location: ICU costs tend to be higher in metropolitan cities compared to smaller towns and rural areas.

- Treatment Complexity: The severity of the illness and the level of care required (e.g., ventilator support, dialysis) significantly impact ICU expenses.

- Duration of Stay: Longer ICU stays naturally lead to higher costs.

ICU Cost Range Across Different City Tiers in India

The cost of ICU stays can vary widely depending on the city tier and the type of room chosen. Below is a breakdown of the average daily costs for different room categories across Tier 1, Tier 2, and Tier 3 cities:

Table

| Room Category | Tier 1 City (Metro) | Tier 2 City | Tier 3 City |

| ICU (Intensive Care Unit) | ₹8,000 – ₹20,000 per day | ₹6,000 – ₹15,000 per day | ₹5,000 – ₹12,000 per day |

| NICU (Neonatal Intensive Care Unit) | ₹5,000 – ₹15,000 per day | ₹4,000 – ₹12,000 per day | ₹3,000 – ₹10,000 per day |

Note: The costs mentioned in the table include charges for nursing, oxygen, and monitoring. These are integral components of the care provided in the ICU and NICU and are reflected in the overall cost.

Disclaimer

These ranges provide a general idea of the potential costs one might incur during an ICU stay. It’s important to note that actual costs may vary based on the specific hospital and the level of care required.

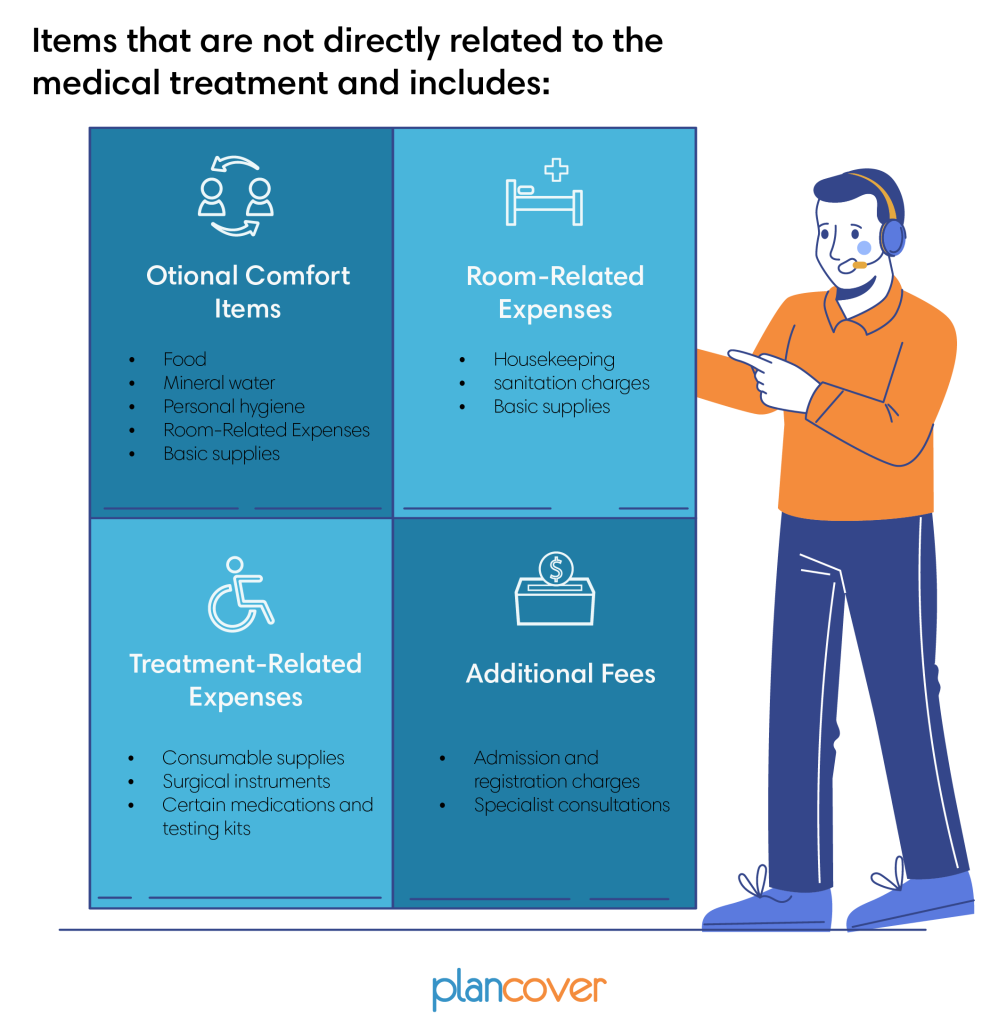

Non-Medical and Consumable Items Excluded from ICU Coverage

When it comes to ICU charges, health insurance policies generally exclude certain non-medical and consumable items from coverage. These items are not directly related to the medical treatment and include:

- Optional Comfort Items:

- Food (beyond hospital-provided meals)

- Mineral water

- Baby-related items (if applicable)

- Personal hygiene and comfort items (toiletries, slippers, etc.)

- Room-Related Expenses

- Housekeeping and sanitation charges

- Basic supplies (tissue paper, hand wash, etc.)

- Treatment-Related Expenses

- Consumable supplies (bandages, syringes, blades)

- Surgical instruments (drills, scalpels)

- Certain medications and testing kits

- Additional Fees

- Admission and registration charges

- Specialist consultations (e.g., nutritionist)

.

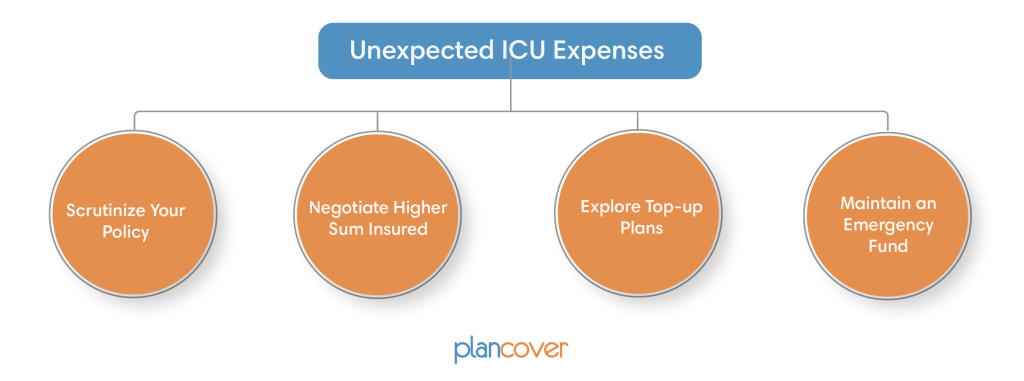

Protecting Yourself from Unexpected ICU Expenses

- Scrutinize Your Policy: Meticulously examine your health insurance policy documents, focusing on the ICU capping provisions for both retail and group plans (if applicable).

- Negotiate Higher Sum Insured (Retail Plans): If feasible, consider increasing your sum insured while purchasing a retail health insurance plan. This provides a larger buffer for potential ICU charges.

- Explore Top-up Plans: For both retail and group plans, explore options for top-up health insurance plans. These offer additional coverage beyond your base policy’s limit, often extending to ICU expenses.

- Maintain an Emergency Fund: Having a contingency fund is essential for unforeseen medical costs that might not be entirely covered by your insurance.

Highlights

- ICU capping is a common feature in both retail and group health insurance plans in India.

- Understanding your policy’s ICU capping limits is crucial to being financially prepared for potential ICU stays.

- Group health plans may offer pre-negotiated lower ICU charges due to insurance company contracts with hospitals. However, confirm specific ICU capping details within your plan.

- Consider increasing your sum insured (retail plans) and explore top-up plans for additional coverage.