Exploring the Corporate Buffer in Group Mediclaim Policies

Group health insurance, often called Group Mediclaim, is a popular employee benefit.

Companies, trade unions, and other recognized groups can purchase these plans to cover their members’ medical expenses.

The specific features of a group health insurance plan will vary depending on the organization’s budget and overall philosophy towards employee benefits. However, many companies offer an additional layer of protection called a corporate buffer

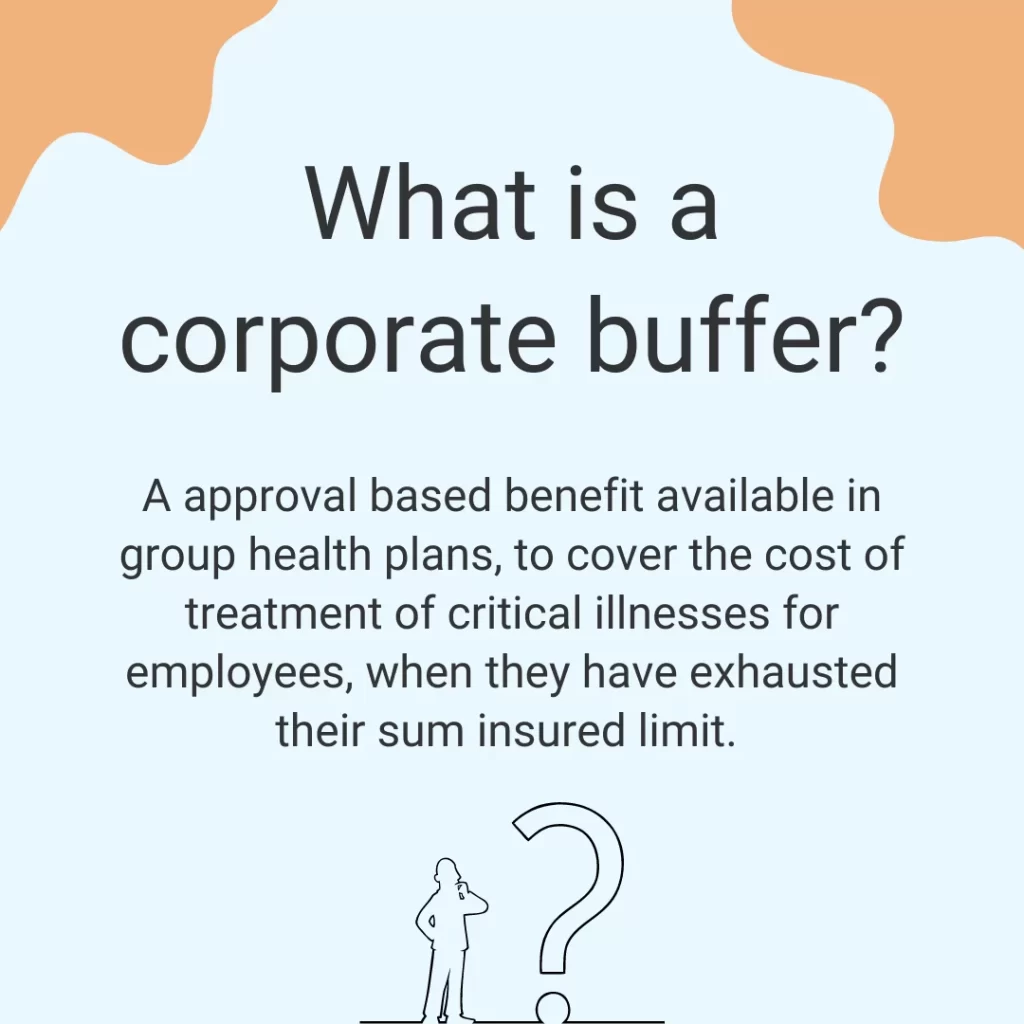

What is a Corporate Buffer?

A corporate buffer acts as a supplementary layer of financial protection within a group health insurance policy. It kicks in when the standard coverage limits of the main policy are reached. This additional buffer provides employees with access to a wider range of healthcare options and minimizes financial burdens during medical emergencies.

Modes of Availing a Corporate Buffer Claim

There are two primary ways to file a claim under a corporate buffer policy:

- Cashless: This mode offers a hassle-free experience. You can seek treatment at network hospitals empanelled with the insurance company. The hospital will directly coordinate with the insurer for claim processing, eliminating upfront payments from your end.

- Reimbursement: In this scenario, you initially bear the hospitalization expenses. After discharge, you submit the required documents to your employer for reimbursement, allowing you to reclaim the covered costs.

Some organizations also offer medical cards that streamline the cashless claim process for employees and their families.

What is Covered under a Corporate Buffer?

While specific coverage details may vary depending on your employer’s policy, corporate buffers typically cover a range of medical expenses, including:

- Inpatient hospitalization charges (room rent, surgeon fees, etc.)

- Medications prescribed during hospitalization

- Diagnostic tests

- Ambulance services

Critical Illness Coverage:

Some corporate buffer plans may also extend coverage to critical illnesses like heart attacks, cancer, or organ failure. These conditions often require expensive treatments, and the buffer can help bridge the gap if the main policy’s coverage limits are insufficient.

What’s Not Covered?

It’s crucial to understand exclusions within your corporate buffer policy. Here are some common exclusions:

- Maternity Expenses: Maternity-related ailments may or may not be covered, depending on your employer’s discretion.

- Exceeding Coverage Limits: The buffer has a pre-defined financial limit. If treatment costs surpass this limit, you’ll be responsible for the additional expense.

- Room Charges: Plans often have a pre-set limit on room rent. If your chosen room exceeds this limit, you’ll bear the difference.

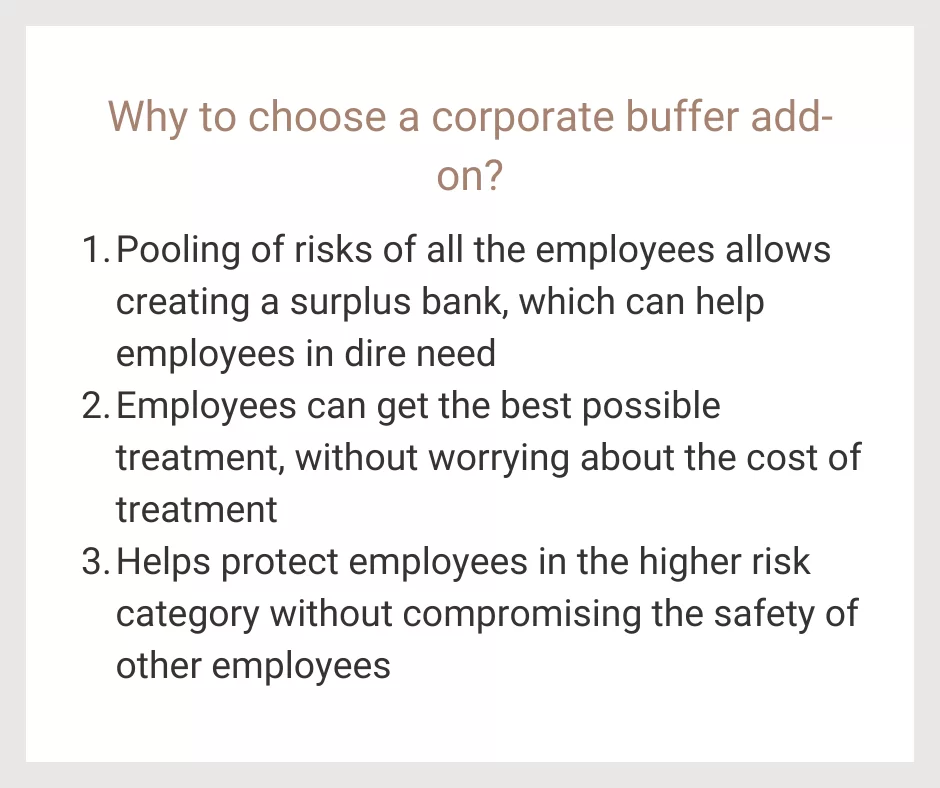

Understanding the Benefits of a Corporate Buffer

Here’s how a corporate buffer can benefit you as an employee:

- Extended Coverage Limits: The buffer acts as a safety net, offering access to higher coverage limits for medical expenses compared to the standard group policy.

- Enhanced Well-being: By reducing the financial burden associated with major illnesses, the buffer contributes to your overall well-being and allows you to focus on recovery.

- Competitive Employer Benefit: A company offering a corporate buffer can enhance its health insurance package, making it more attractive to potential recruits and promoting employee retention.

Scenarios Where a Corporate Buffer is Valuable

Corporate buffers prove particularly valuable in situations like:

- Major surgeries: These procedures can easily exhaust standard coverage limits. The buffer ensures access to necessary procedures without financial worries.

- Prolonged Hospitalization: Extended hospital stays can quickly deplete the main policy’s coverage. The buffer steps in to minimize the financial burden during this time.

- Expensive Treatments: Certain treatments, such as cancer therapies, can be expensive. The buffer provides additional financial support to cover these costs.

Limitations and Considerations

Corporate buffers aren’t limitless resources. Employers need to carefully plan and periodically assess the buffer funds to ensure their alignment with the evolving healthcare needs of their workforce.

Strategic Use of Corporate Buffer

Optimizing the effectiveness of the corporate buffer involves strategically incorporating it into the overall health insurance policy design. Customizing the buffer to address specific health risks prevalent within the employee population allows for a more targeted and impactful approach.