Co-Pay in Indian Health Insurance: A Comprehensive view

Introduction

Choosing the right health insurance plan is essential to protect yourself and your loved ones from unexpected medical expenses. One critical concept to understand is “co-pay,” as it directly impacts your out-of-pocket costs. This comprehensive guide will break down co-pay, its different forms, advantages, disadvantages, and how it works within your insurance plan.

What is Co-Pay ?

Copay, also referred to as a copayment, indeed plays a crucial role in the realm of healthcare expenses. When an individual seeks medical services, they are required to contribute a predetermined fixed amount, while the insurance company covers the remaining portion

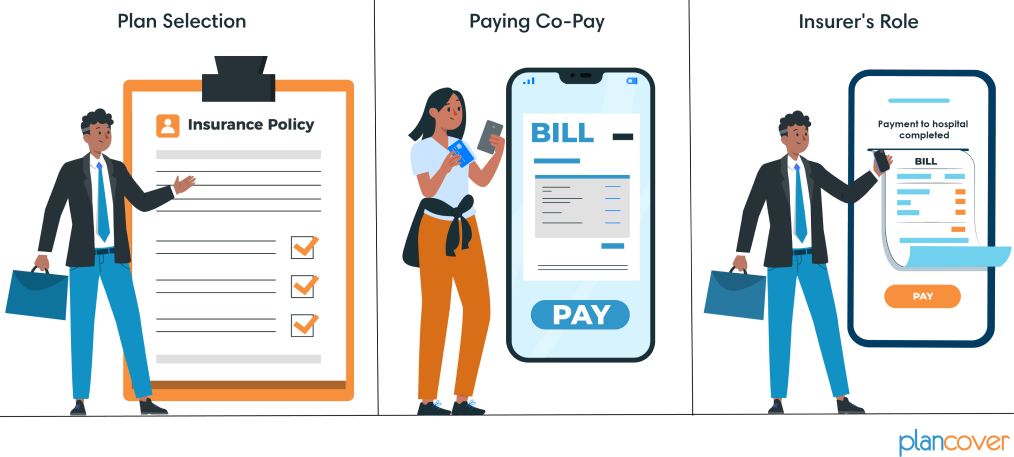

How Does Co-Pay Work in Indian Health Insurance?

Plan Selection: When you choose a health insurance policy, some plans include a co-pay feature while others may not.

Paying Co-Pay: If you receive treatment, you’ll directly pay the fixed co-pay amount to the hospital or healthcare provider.

Insurer’s Role: Your healthcare provider then bills your insurer for the remaining amount of the medical expenses.

For instance, with a 20% co-pay clause and a claim of ₹1,00,000, the policyholder would contribute ₹20,000, while the insurer covers the remaining ₹80,000.

Co-pay vs Deductible vs Coinsurance: Deciphering the Differences

Navigating the world of health insurance can be complex, especially when it comes to understanding terms like co-pay, deductible, and coinsurance. These are key components of any health insurance policy and understanding them is crucial to making the most of your coverage.

Co-pay

A co-pay is a fixed amount you pay for each medical service. It’s usually a small amount that you pay out-of-pocket each time you visit a doctor, get a prescription filled, or use other healthcare services.

Illustration: Let’s say you have a plan with a ₹1,500 co-pay for doctor visits. Each time you visit your doctor, you pay ₹1,500 out-of-pocket, and your insurance covers the rest.

Deductible

A deductible is the amount an individual pays out-of-pocket before the insurance company begins covering the cost of medical services. It’s like a threshold that you need to meet each year before your insurance starts to pay.

Illustration: Suppose you have a plan with a ₹50,000 annual deductible. For the first ₹50,000 of medical expenses each year, you pay the full cost. Once you’ve met the deductible, your insurance starts to cover eligible costs.

Coinsurance

Coinsurance is the percentage of the cost of medical services that an individual is responsible for paying after meeting their deductible. It’s can be said that it is combination of co-pay and deductible

Illustration: an individual has a health insurance plan with a Rs 5,000 deductible and a 10% co-insurance requirement. If the person undergoes a healthcare service that costs Rs 10,0000, he/she would be responsible for paying the first Rs 5,000 (the deductible). After that, the person would be responsible for paying 10% of the remaining Rs 95,000, or Rs 85,500. The insurance provider would cover the remaining amount.

Exploring the Co-Payment Feature in Health Insurance Policies

Benefits for Policyholders and Insurers:

- Shared Expenses: The co-payment feature introduces a shared payment model, easing the financial load for both the insured and the insurer.

- Reduced Premiums: Policies incorporating co-payment typically offer the advantage of reduced premium costs.

- Mindful Medical Service Use: Co-payment encourages judicious use of medical services, curbing unnecessary medical expenditures.

- Foreseeable Medical Expenditures: With co-payment, policyholders have a clearer understanding of their expected medical costs.

- Network Provider Incentives: Policies may offer reduced co-payment rates for using preferred network providers, promoting cost-effective healthcare choices.

Challenges Associated with Co-Payment: - Increased Direct Costs: Co-payment can lead to higher immediate healthcare costs for policyholders, particularly for those requiring regular medical attention.

- Coverage Restrictions: Certain policies may not apply the co-payment feature to all services, potentially resulting in full out-of-pocket costs for some treatments.

- Complexity in Understanding: The intricacies of co-payment clauses can be challenging to grasp, leading to potential confusion regarding financial responsibilities.

- Potential Deterrent to Seeking Care: The added expense of co-payment might discourage individuals from obtaining necessary medical services, possibly affecting health outcomes negatively.

- Administrative Complexity: The implementation of co-payment adds layers of administrative processes, which could elevate the overall costs of health insurance policies.

Co-Pay Clauses in Health Insurance Policies

Health insurance policies often include co-pay clauses, which determine the portion of medical expenses that policyholders must pay out of their own pockets. These clauses can vary based on factors such as age, location, and hospital choice. Let’s explore the common types of co-pay clauses in health insurance:

- Age-related Clause: This type of copay clause is based on the insured person’s age. As individuals age, they are more likely to require medical treatment, which can result in higher insurance costs for the insurer. Therefore, insurance policies may include copay requirements that increase with age to help mitigate this risk.

Illustration: Mr. Sharma’s Age-Related Co-Pay Scenario (with Age Consideration):

● Profile: Mr. Sharma, a 65-year-old retiree.

● Health Insurance Policy: Mr. Sharma holds a health insurance policy that includes an age-related co-pay clause.

● Starting Age for Co-Pay: The age at which the co-pay clause becomes applicable is typically specified in the policy. Let’s assume it starts at age 60.

Now, let’s break down the financial implications:

- Age Threshold Reached:

▪ Upon turning 60, Mr. Sharma becomes subject to the age-related co-pay clause in his policy. - Medical Procedure and Hospital Bill:

▪ Suppose Mr. Sharma undergoes a medical procedure covered by his policy, resulting in a hospital bill of ₹50,000. - Co-Pay Requirement:

▪ The co-pay requirement specified in his policy is 20%. - Mr. Sharma’s Contribution:

▪ Co-Pay Percentage: 20%

▪ Amount Mr. Sharma Pays: ₹50,000 × 20% = ₹10,000 - Insurer’s Coverage:

▪ Amount Covered by Insurer: ₹50,000 − ₹10,000 = ₹40,000

In this revised scenario, Mr. Sharma pays ₹10,000 out of his own pocket, while the insurer covers the remaining ₹40,000. The age-related co-pay clause ensures that as individuals age, they contribute a portion of the claim amount, helping insurers manage risks associated with higher healthcare costs for seniors.

- Age Threshold Reached:

Hospital-related Clause: Some insurance policies may impose copay clauses based on where the insured individual receives treatment. If treatment is received at a non-network hospital that is not affiliated with the insurer, a copay may be required for reimbursement claims. However, cashless claims at network hospitals may not be subject to copay provisions.

Illustration :

Mr. Sharma, a 45-year-old professional, holds a comprehensive health insurance policy. His plan includes a hospital-related co-pay clause. Here’s how it works:

- Non-Network Hospital (Scenario A):

▪ Mr. Sharma pays ₹15,000 (15% co-pay) out of his own pocket.

▪ Insurer covers ₹85,000. - Network Hospital (Scenario B):

▪ Mr. Sharma enjoys a seamless cashless process.

▪ No co-pay required.

Medical Conditions-related Clause:

Copay clauses may also be applied to specific medical conditions or treatments that are known to be expensive. For example, copays may be required for treatments related to critical illnesses or pre-existing conditions. This helps insurers manage the costs associated with covering these conditions.

Illustration :Scenario: Critical Illness Treatment

● Profile: Ms. Patel, a 50-year-old policyholder.

● Health Condition: Unfortunately, Ms. Patel is diagnosed with a critical illness (e.g., cancer, heart disease, or kidney failure).

● Treatment Cost: The medical expenses for her treatment amount to ₹5,00,000.

● Co-Pay Requirement: Her health insurance policy includes a medical conditions-related co-pay clause of 10% for critical illnesses.

Now, let’s break down the financial implications:

- Ms. Patel’s Contribution:

▪ Co-Pay Percentage: 10%

▪ Amount Ms. Patel Pays: ₹5,00,000 × 10% = ₹50,000 - Insurer’s Coverage:

▪ Amount Covered by Insurer: ₹5,00,000 − ₹50,000 = ₹4,50,000

In this scenario, Ms. Patel pays ₹50,000 out of her own pocket, while the insurer covers the remaining ₹4,50,000. The medical conditions-related co-pay clause ensures that policyholders share the burden of expensive treatments, allowing insurers to manage costs effectively.

Location-related Clause: Insurance policies may include copay clauses that vary based on the geographic location where medical services are received. Medical expenses tend to be higher in major cities compared to smaller towns or rural areas. Therefore, insurers may impose copay provisions to account for this difference in cost.

Illustration: Urban vs. Rural Healthcare Costs

● Profile: Mr. Rao, a 40-year-old business owner.

● Health Condition: Mr. Rao requires a minor surgery.

● Treatment Location:

▪ Urban Scenario (Major City):

Mr. Rao opts for a hospital in a major city (e.g., Hyderabad or Chennai) for his surgery.

The total medical expenses amount to ₹1,20,000.

Co-Pay Percentage: 12% (as per his policy).

Mr. Rao pays: ₹1,20,000 × 12% = ₹14,400.

Insurer covers: ₹1,05,600.

Rural Scenario (Smaller Town):

Alternatively, if Mr. Rao chooses a hospital in a smaller town (rural area), he incurs lower expenses.

No co-pay provisions apply due to the cost advantage.

Insurer covers the entire bill.

Voluntary Co-Pays: Some policies let you choose to add a co-pay in exchange for lower premiums. This depends on your risk tolerance and how much you want to potentially pay out-of-pocket.

These copay clauses help insurers manage risk and control costs while providing coverage to policyholders. It’s important for individuals to review their insurance policies carefully to understand any copay requirements that may apply to them.

Parental Co-Pay in Indian Health Insurance

Parental co-pay is a specialized component within health insurance policies in India, addressing the unique healthcare needs of ageing parents. This feature tailors co-payment clauses specifically for parents, considering their heightened health risks.

Understanding Parental Co-Pay

Parental co-pay mirrors standard co-pay structures, establishing a cost-sharing agreement between policyholders and insurers. However, parental co-pay typically involves a higher percentage compared to other members within the policy, recognizing the increased health risks and potential medical expenses associated with elderly individuals.

Illustrations

Co-Pay Structure Chart: A table showing examples of co-pays for different Policy Type

| Insurance Type | Beneficiary | Co-Pay Percentage | Remarks |

| Retail Health Insurance | Immediate Family Members | 10-20% | Co-pay percentages can differ based on the service and plan specifics. |

| Parents | 20-30% | Co-pay percentages for parents are often higher due to increased health risks associated with age. | |

| Group Health Insurance | Immediate Family Members | 5-15% | Employers may negotiate different co-pay rates for their employees’ families. |

| Parents | 15-25% | Some employers may offer plans with special conditions for parental coverage, potentially with different co-pay rates. |

Insurance Type Beneficiary Co-Pay Percentage Remarks

Retail Health Insurance Immediate Family Members 10-20% Co-pay percentages can differ based on the service and plan specifics.

Parents 20-30% Co-pay percentages for parents are often higher due to increased health risks associated with age.

Group Health Insurance Immediate Family Members 5-15% Employers may negotiate different co-pay rates for their employees’ families.

Parents 15-25% Some employers may offer plans with special conditions for parental coverage, potentially with different co-pay rates.

These percentages are indicative and based on the typical range found in the market. The actual co-pay percentages and terms will depend on the specific health insurance policy and the insurer’s terms and conditions.

Grasping the implications of co-pay clauses in health insurance policies is pivotal for making informed decisions. Thoroughly reviewing policy documents and seeking clarification from insurers ensures that health insurance coverage aligns with individual needs, offering comprehensive protection against unforeseen medical expenses.